题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

提问人:网友lihuinihao

发布时间:2022-01-07

[主观题]

A two-year floating-rate note pays 6-month Libor plus 80 basis points. The floater is pric

ed at 97 per 100 of par value. Current 6-month Libor is 1.00%. Assume a 30/360 day-count convention and evenly spaced periods. The discount margin for the floater in basis points is closest to

A、180 bps

B、236 bps

C、420 bps

D、空

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

查看官方参考答案

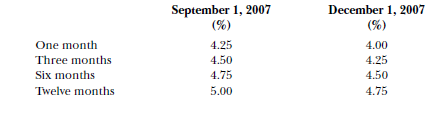

a. What is the coupon paid on September 1, 2007, per $1,000 FRN? b. What is the new value of the coupon set on the FRN on September 1, 2007? c. What is the new value of the FRN on December 1, 2007?

a. What is the coupon paid on September 1, 2007, per $1,000 FRN? b. What is the new value of the coupon set on the FRN on September 1, 2007? c. What is the new value of the FRN on December 1, 2007?