题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

提问人:网友tmwlnjtu

发布时间:2022-01-06

[主观题]

If Trial 4 had been extended, at approximately what time would 0.45 mL of 0 2 have reacted

?

A.70 sec

B.140 sec

C.240 sec

D.270 sec

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

查看官方参考答案

题目内容

(请给出正确答案)

A.70 sec

B.140 sec

C.240 sec

D.270 sec

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

更多“If Trial 4 had been extended, at approximately what time would 0.45 mL of 0 2 have reacted”相关的问题

更多“If Trial 4 had been extended, at approximately what time would 0.45 mL of 0 2 have reacted”相关的问题

A.less than 1.86 sec.

B.between 1.86 sec and 1.93 sec.

C.between 1.94 sec and 1.96 sec.

D.greater than 1.96 sec.

Q’s trial balance failed to agree and a suspense account was opened for the difference. Q does not keep receivables and payables control accounts. The following errors were found in Q’s accounting records: (1) In recording an issue of shares at par, cash received of $333,000 was credited to the ordinary share capital account as $330,000 (2) Cash of $2,800 paid for plant repairs was correctly accounted for in the cash book but was credited to the plant asset account (3) The petty cash book balance of $500 had been omitted from the trial balance (4) A cheque for $78,400 paid for the purchase of a motor car was debited to the motor vehicles account as $87,400. Which of the errors will require an entry to the suspense account to correct them?

A、1, 2 and 4 only

B、1, 2, 3 and 4

C、1 and 4 only

D、2 and 3 only

The following information is relevant for questions 9 and 10

A company’s draft financial statements for 2005 showed a profit of $630,000. However, the trial balance did not agree,

and a suspense account appeared in the company’s draft balance sheet.

Subsequent checking revealed the following errors:

(1) The cost of an item of plant $48,000 had been entered in the cash book and in the plant account as $4,800.

Depreciation at the rate of 10% per year ($480) had been charged.

(2) Bank charges of $440 appeared in the bank statement in December 2005 but had not been entered in the

company’s records.

(3) One of the directors of the company paid $800 due to a supplier in the company’s payables ledger by a personal

cheque. The bookkeeper recorded a debit in the supplier’s ledger account but did not complete the double entry

for the transaction. (The company does not maintain a payables ledger control account).

(4) The payments side of the cash book had been understated by $10,000.

9 Which of the above items would require an entry to the suspense account in correcting them?

A All four items

B 3 and 4 only

C 2 and 3 only

D 1, 2 and 4 only

Eight foreign aid workers were arrested in Afghanistan because of their ______ activities.

A.political

B.espionage

C.religious

D.relief

A.intrepid...valiant

B.guileless...hypocritical

C.abstemious...temperate

D.meek...timorous

E.ingenuous...obtuse

A.electrons;protons

B.protons;electrons

C.electrons;electrons

D.protons;protons

A.34°C.

B.42°C.

C.50°C.

D.62°C.

A.DR $210

B.CR $210

C.DR $160

D.CR $160

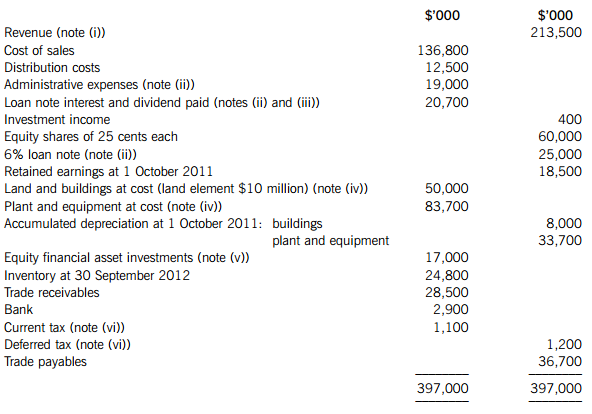

The following trial balance relates to Quincy as at 30 September 2012:

The following notes are relevant:

(i) On 1 October 2011, Quincy sold one of its products for $10 million (included in revenue in the trial balance). As part of the sale agreement, Quincy is committed to the ongoing servicing of this product until 30 September 2014 (i.e. three years from the date of sale). The value of this service has been included in the selling price of $10 million. The estimated cost to Quincy of the servicing is $600,000 per annum and Quincy’s normal gross profit margin on this type of servicing is 25%. Ignore discounting.

(ii) Quincy issued a $25 million 6% loan note on 1 October 2011. Issue costs were $1 million and these have been charged to administrative expenses. The loan will be redeemed on 30 September 2014 at a premium which gives an effective interest rate on the loan of 8%.

(iii) Quincy paid an equity dividend of 8 cents per share during the year ended 30 September 2012.

(iv) Non-current assets:

Quincy had been carrying land and buildings at depreciated cost, but due to a recent rise in property prices, it decided to revalue its property on 1 October 2011 to market value. An independent valuer confirmed the value of the property at $60 million (land element $12 million) as at that date and the directors accepted this valuation. The property had a remaining life of 16 years at the date of its revaluation. Quincy will make a transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation reserve. Ignore deferred tax on the revaluation.

Plant and equipment is depreciated at 15% per annum using the reducing balance method.

No depreciation has yet been charged on any non-current asset for the year ended 30 September 2012. All depreciation is charged to cost of sales.

(v) The investments had a fair value of $15·7 million as at 30 September 2012. There were no acquisitions or disposals of these investments during the year ended 30 September 2012.

(vi) The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2011. A provision for income tax for the year ended 30 September 2012 of $7·4 million is required. At 30 September 2012, Quincy had taxable temporary differences of $5 million, requiring a provision for deferred tax. Any deferred tax adjustment should be reported in the income statement. The income tax rate of Quincy is 20%.

Required:

(a) Prepare the statement of comprehensive income for Quincy for the year ended 30 September 2012.

(b) Prepare the statement of changes in equity for Quincy for the year ended 30 September 2012.

(c) Prepare the statement of financial position for Quincy as at 30 September 2012. Notes to the financial statements are not required.

The following mark allocation is provided as guidance for this question:

(a) 11 marks

(b) 4 marks

(c) 10 marks

A、Debit $210

B、Credit $210

C、Debit $160

D、Credit $160

警告:系统检测到您的账号存在安全风险

警告:系统检测到您的账号存在安全风险

为了保护您的账号安全,请在“简答题”公众号进行验证,点击“官网服务”-“账号验证”后输入验证码“”完成验证,验证成功后方可继续查看答案!