题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

提问人:网友woainba

发布时间:2022-01-07

[单选题]

【单选题】Interest Rate Swap是 ()

A.利率互换

B.货币互换

C.伦敦同业拆借

D.上海同业拆借

参考答案

参考答案

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

查看官方参考答案

网友提供的答案

网友提供的答案

共位网友提供了参考答案,

查看全部

- · 有4位网友选择 C,占比44.44%

- · 有2位网友选择 D,占比22.22%

- · 有2位网友选择 B,占比22.22%

- · 有1位网友选择 A,占比11.11%

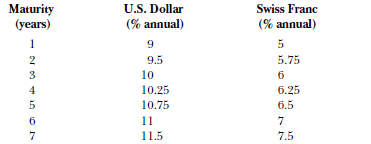

a. Calculate the swap payments at the end of the fourth year (i.e., today). b. Right after this payment, what is the market value of the swap to the Swiss firm?

a. Calculate the swap payments at the end of the fourth year (i.e., today). b. Right after this payment, what is the market value of the swap to the Swiss firm?