3 You are the manager responsible for the audit of Albreda Co, a limited liability company

, and its subsidiaries. The

group mainly operates a chain of national restaurants and provides vending and other catering services to corporate

clients. All restaurants offer ‘eat-in’, ‘take-away’ and ‘home delivery’ services. The draft consolidated financial

statements for the year ended 30 September 2005 show revenue of $42·2 million (2004 – $41·8 million), profit

before taxation of $1·8 million (2004 – $2·2 million) and total assets of $30·7 million (2004 – $23·4 million).

The following issues arising during the final audit have been noted on a schedule of points for your attention:

(a) In September 2005 the management board announced plans to cease offering ‘home delivery’ services from the

end of the month. These sales amounted to $0·6 million for the year to 30 September 2005 (2004 – $0·8

million). A provision of $0·2 million has been made as at 30 September 2005 for the compensation of redundant

employees (mainly drivers). Delivery vehicles have been classified as non-current assets held for sale as at 30

September 2005 and measured at fair value less costs to sell, $0·8 million (carrying amount,

$0·5 million). (8 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Albreda Co for the year ended

30 September 2005.

NOTE: The mark allocation is shown against each of the three issues.

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

参考答案

参考答案

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

简答题官方参考答案

(由简答题聘请的专业题库老师提供的解答)

网友提供的答案

网友提供的答案

,

, ,欲完成两个多项式相加、相乘和相除

,欲完成两个多项式相加、相乘和相除 的运算,则以下哪个程序正确?

的运算,则以下哪个程序正确?

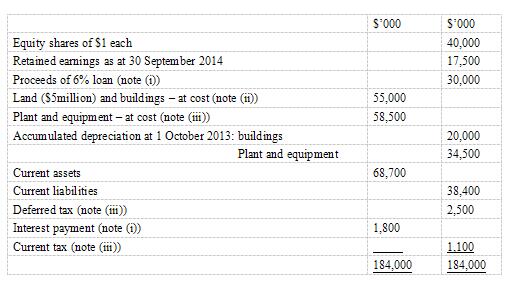

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.

(i)The loan note was issued on 1 October 2013 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1·8 million ($30 million at 6%) was paid on 30 September 2014. The loan is redeemable on 30 September 2018 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 2018.